Tri-Cities isn’t facing real estate bubble

By Dennis Gisi

Is it really a seller’s real estate market?

Yes!

Why?

The reason is somewhat lengthy and complicated.

Dennis Gisi,

Dennis Gisi,

I am going to start with a 1999 New York Times article written by Steven H. Holmes published in the New York Times, entitled, “Fannie Mae eases credit to aid mortgage lending.” The story refers to the political maneuvering by the Clinton Administration to increase homeownership in this country. The administration was in its second term and looking for what its legacy could or should be. One key component was to increase homeownership in the country, particularly with those who had poor credit or limited incomes.

According to the article, two government sponsored enterprises succumbed to the political pressure of the administration: Fannie Mae and Freddie Mac. Under the order of Congress and through the Department of Housing and Urban Development’s relaxed credit standards, they were directed to include subprime loans in Fannie Mae’s portfolio.

By 2007, Fannie and Freddie were required to show 55 percent of their mortgage purchases were lenders’ mortgage insurance, or LMI, loans and, within that goal, 38 percent of all purchases were to come from underserved areas (usually inner cities) and 25 percent were to be loans to low-income and very low-income borrowers. Meeting these goals almost certainly required Fannie and Freddie to purchase loans with low down payments and other deficiencies that would mark them as sub-prime, according to “The true story of the financial crisis” by The American Spectator.

CNN Money reported in December 2008 the losses of Fannie Mae alone were estimated to be $29 billion. As we now know, the losses would continue.

Closer to home, as reported by American Banker in 2010, financial losses forced the Federal Housing Finance Agency to enter into a consent order with the Federal Home Loan Bank of Seattle under the direction of Richard M. Riccobono, currently supervisor of banks for the Washington State Deptarment of Financial Institutions, to improve its capital position and business and operations.

Simultaneously, the bank announced that Riccobono, its president and chief executive, had resigned. His losses during that time were so large that the end result was a merger of the Seattle Bank with the Federal Home Loan Bank of Des Moines in 2014.

The pendulum swings in both directions. Now the regulations that were proposed by Congress directing regulators of the Federal Deposit Insurance Corp. and Office of the Comptroller of the Currency to ensure banks comply are scrambling to enforce new rules and regulations to undo their wrongdoing and enforce stricter capital requirements and avoid any risk.

One area regulators watched extremely closely and criticized was acquisition and development loans for new residential construction. Developers without this source of funding could not acquire land and further its development into residential lots. Eventually the supply of lots that had been available shrank and inventory of homes for sale fell to an all-time low.

It was recently reported that the Tri-Cities is the 18th fastest growing MSA (Metropolitan Statistical Area) in the country. We see new development everywhere. Has the spigot of money been turned back on?

No, local developers are using their own money, private sources or hard money lenders to obtain the money necessary to develop property. Today, I know of only one local bank that MIGHT consider funding an acquisition and development project.

No, local developers are using their own money, private sources or hard money lenders to obtain the money necessary to develop property. Today, I know of only one local bank that MIGHT consider funding an acquisition and development project.

The result is we are seeing land prices being bid up dramatically by builders and developers to acquire enough land to continue to build supply and meet the demand of home buyers in our area.

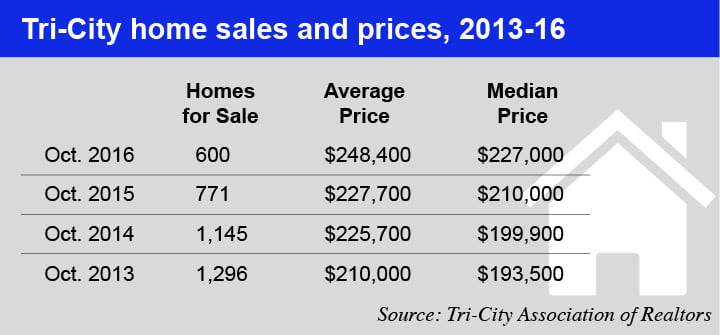

Recent data from the Tri-City Association of Realtors shows that without the availability of money to continue the growth to meet demand, the number of homes available is near an all-time low and housing prices measured by both the average and median prices have gone up to pay for the increases in the price of land and other building materials.

American business icon and philanthropist, and CEO of Berkshire Hathaway, Warren Buffett was asked earlier this year if we are in a housing bubble. His answer: No.

For the Tri-Cities, I would agree with Mr. Buffett. I would also ask those in control of the flow of money to open the money spigot and let a prudent flow be directed to the housing industry, particularly here in the Tri-Cities.

Dennis Gisi is the owner of John L. Scott in Pasco. Gisi is also the retired president, CEO and a former chairman of Bank Reale in Pasco.